“In a society marked by the respect for freedom….. citizens are under no obligation, barring good reasons, to disclose what they do in their free time, which books they buy, which newspapers they subscribe to, what they eat and drink, and where they spend the night. Even though such matters are not usually kept secret and, depending on the circumstances, easily become known to a limited group of people, it is at the discretion of the person concerned to decide whether he/she is willing to disclose such information, which information it will be and to whom it will be disclosed. This also holds for an entirely inconspicuous private life.” This clear statement by the Constitutional Court is contained in its decision to repeal certain provisions of the Vienna Entertainment Tax Act (14 March 1991, VfSlg 12.689), which required operators of videotheques to keep detailed records of their customers’ patterns of use.

In 1986 and 1987, the Vienna Provincial Parliament decided to impose entertainment tax on the renting of film video cassettes, commonly called “video lending”. While cinema tickets had long been subject to such tax, it was now decided, for reasons of fair competition, to impose the tax also on video cassette rental. The tax was designed as a direct tax imposed on the borrower but to be collected and remitted to the tax authority by the videotheque operators. The latter were liable for payment of the tax and, additionally, were required to “keep records indicating, at any point in time, the operator’s stock of programme storage media and films as well as when, by whom, for how long and at which price a programme storage medium or film was rented”, this being the provision at issue in the case brought before the Constitutional Court. Apparently, the Municipality of Vienna had perceived a risk of untaxed video rentals and the avoidance by traders of taxation on parts of their income.

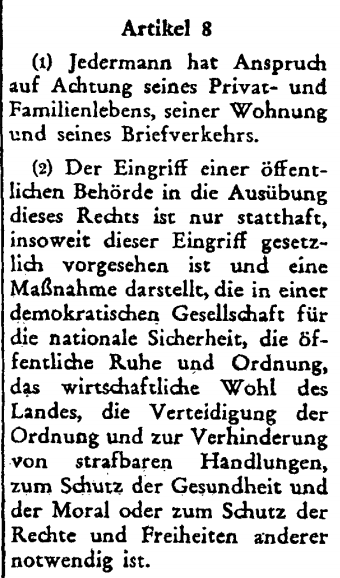

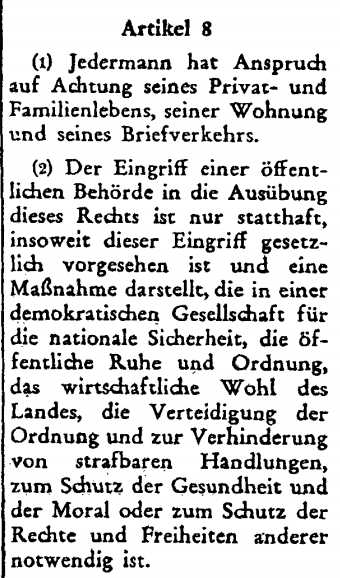

Given that the Constitutional Court regarded the comprehensive disclosure and recording obligations as inseparably linked with the obligation to pay tax, it excluded the renting of video cassettes from entertainment tax altogether. The judges deemed the tax, in the form imposed, to constitute an infringement of the right to respect for private and family life enshrined in Article 8 of the European Convention on Human Rights (ECHR), “as it entails an interference with a person’s private life, which is unnecessary in order to tap this revenue source…”. The Court ruled that for the tax to fulfil its fiscal purpose, it was not at all necessary to know exactly who rented which film when and where. To underline this position, the Constitutional Court compared the entertainment tax imposed on customers of videotheques with the excise tax on the consumption of ice-cream and beverages: As an indirect tax, the latter was imposed on the sale by the trader rather than on the product’s consumption by the consumer, “without having the tax losing any of its effect, and without making its collection dependent on detailed records indicating to whom the ice-cream was sold or the beverage served.”

In Austria, the ECHR was granted the rank of a constitutional law in 1964 (Federal Law Gazette No. 59/1964). The Vienna entertainment tax was abolished once and for all in 2017, due to the fact that revenues from this tax had decreased sharply. Meanwhile, videotheques have almost completely disappeared, given that video cassettes, CD-ROMs and Blu-rays have been replaced by the Internet.